Medical network - January 10, according to the m Intranet "key urban retail pharmacies proprietary Chinese medicine terminal competition", according to a 2015 key cities for the retail pharmacies proprietary Chinese medicine market scale almost fifty percent in the first three categories of proprietary Chinese medicine market.

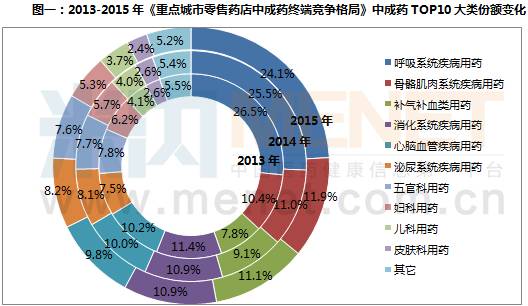

The respiratory system diseases accounted for 24.1%. A declining share in 2013-2015, musculoskeletal system disease drugs accounted for 11.9%, increased share from the previous two years, fill gas blood tonic medicine accounted for 11.1%, 2013-2015 market share continue to rise, urinary system disease drug market proportion is rising trend, accounted for the rest of the categories are slightly down.

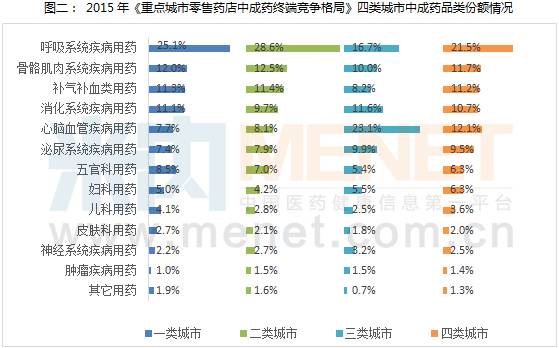

From four types of cities, category, type of second city belongs to the high level of consumption of cities, this kind of urban retail proprietary Chinese medicine category structure is similar to that of the first five categories, in turn, drug for respiratory system diseases, diseases of the musculoskeletal system drugs, fill gas blood tonic medicine, diseases of the digestive system drugs and disease of heart head blood-vessel drug use.

Three or four class cities belong to the consumption level is relatively weak, on the drug structure with one, second-tier cities have obvious differences, like three cities ranked first cardiovascular drugs, respiratory disease, followed by the third is the diseases of the digestive system drugs.

And the fourth ranked the first class city drug structure though is the respiratory system disease, but the second is disease of heart head blood-vessel, the third and the fourth is the musculoskeletal system disease medication and fill gas blood tonic medicine.

In the city of grade 1 and 2, the floating population is relatively more, young people are relatively more, so common diseases can dominate, and in three or four class city, less liquidity population, population aging, chronic diseases will gradually dominant.

Relatively high consumption level of the city also has a relatively high degree of brand concentration

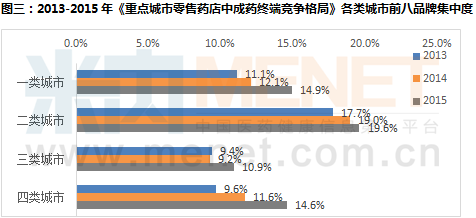

Through the analysis of market concentration, we can see proprietary Chinese medicine retail market competition condition. Analysis of market concentration index is usually industry concentration ratio (CRn), Hector seaman index, lorentz curve and gini coefficient, reverse index, etc., then we will use four types of cities in the first eight brand share in total (CR8) for the analysis of four types of urban drug market situation of brand concentration.

From 2015, four CR8 are less than 20% of the city, is belonging to dispersible competition in the market. Contrast, the second city has the highest degree of market concentration, 19.6%; Three kinds of cities are the lowest, at 10.9%, a class and second class market concentration are around 14.6% of the city.

From here we can find a pattern is a high consumption city market relatively high degree of brand concentration is, the recognition of the brand at a higher, and the low level of consumption of the city market concentration is relatively late, less reliance on brand.

City from 2013 to 2015, four types of proprietary Chinese medicine CR8 retail brands combined trends, all have different degree of brand concentration degree of all kinds of city rise, including four types of cities and city rise higher, at about 2%. As countries increasingly strict regulation of drug, the future market will be out of a batch of competitive weaker medicines, expected market will further concentration degree of brand concentration.

Second city of retail pharmacies in chemical medicine, sales in the first three brands are Pfizer atorvastatin calcium tablet, Pfizer's benzene sulfonic acid amlodipine and bayer acarbose tablets. In addition, sales in the top 10 brands, wyeth sales fastest growing calcium carbonate D3 tablets, compound growth rate of 26.3% in 2013-2013.

High level of consumption city more strong demand for high tonic brand

A, second-tier cities belong to relatively high consumption level, the brand from the category of proprietary Chinese medicine retail market structure and market concentration degree, are similar, so on brand and whether there is any difference?

From the list of the top eight brands, a repeated, second-tier cities degree is higher, there are five brand repeat, only the ranking order is different, respectively is the company of donkey-hide gelatin, gelatin, hong MAO medicated wine, Kyoto CiAn honey refined fritillary bulb become pipagao in kidney with hui ren treasure.

City of grade 1 and 2, significant difference is the number one product tin maple particles (zhejiang pharmaceutical the emperor), its sales with a strong regional, second in the second city no medicine XiaoTong adminstration of market position is obviously higher than that of Inner Mongolia hong MAO pharmaceutical hong MAO medicinal liquor.

Another spleen-invigorating zhejiang love raw pharmaceutical particles in the past two years in the second city also has a good development trend, the compound growth rate of 72.9% in 2013-2015, belongs to one of the high speed development of brand, to be reckoned with in the future development tendency.

|