Medical net June 30, 2008-2017, to change the new medicine to the beginning, is the traditional pattern to end the decade, also is the new ecological decade.

Comes at a time when 2017 heap will heap the coming ten years, the organizers of health information from the data dimension, combing drugs compared before and after ten years of the development of the retail industry, from the data perspective, from the law in the future, multidimensional analytic assembly "focus on the demand of the market awareness building blueprint" the theme of logic.

Ten years, our country medicine retail size increased from 143 billion yuan to 337.7 billion yuan, chain rate rise to 49.4% from 35.3%, in our country people's self-medication and drug accessibility are playing an increasingly important role, with the prescription of outflow trend became clear, drug retail terminal has become increasingly important in the position in national medical health system. However, from the proportion of the top 100, it still lingers around 34%, indicating that the concentration of China's drug retail market is still huge. Before the trillion-dollar market, drug retail is ready to go.

�� size ten years: double size, growth is stabilizing

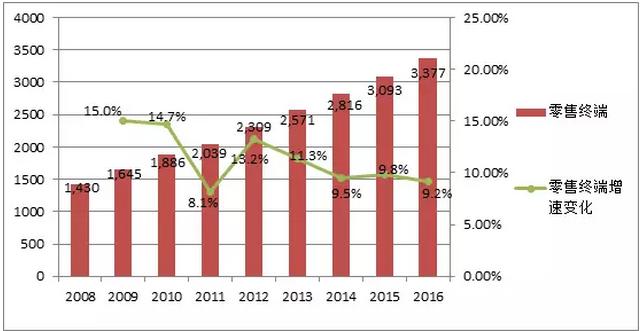

Figure 1: retail terminal market size (unit: billion yuan) and growth rate in 2008 ~ 2016

(source: zhongkang CMH)

With the aging of the population, the awareness of health care of residents and the improvement of the medical care system, China's drug market has expanded rapidly. The national drug market increased from 483.5 billion yuan in 2008 to 14,909 billion yuan in 2016, according to the China kang CMH study.

Specifically, the size of the drug retail terminal market more than doubled between 2008 and 2016, from 143 billion yuan in 2008 to 337.7 billion yuan in 2016. In terms of growth, retail terminals grew rapidly in 2009 and 2010, with year-on-year growth of 15.0% and 14.7% respectively. In the next few years, retail terminal growth stabilizes, and gradually enter weak growth situation.

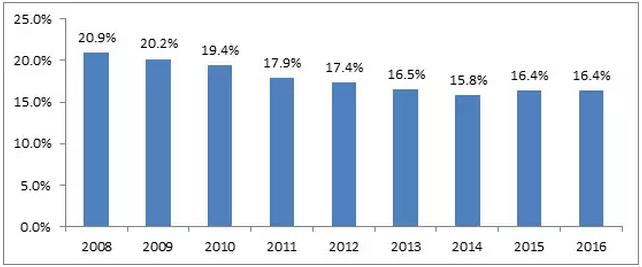

Figure 2. The proportion of drug retail terminal market share in 2008 ~ 2016

(source: zhongkang CMH)

Due to the medical system and other factors, the current hospital terminal still occupies the major drug market share, while the retail terminal account has a small decline. From 2008 to 2009, the market share of drug retail terminals (excluding medicinal materials) accounted for about 20% of the total market share, and the share of the drug market has been hovering around 16% since then, according to the study.

�� concentration for 10 years: oligarchs premature

After the barbaric growth of the pharmaceutical retail industry, began to enter the brand, chain, scale development period. Under the threat of a capital boom, some powerful chains have opened their capital and expanded their sphere of influence. But it is a long way from a two-thirds target.

1. Linkage rate

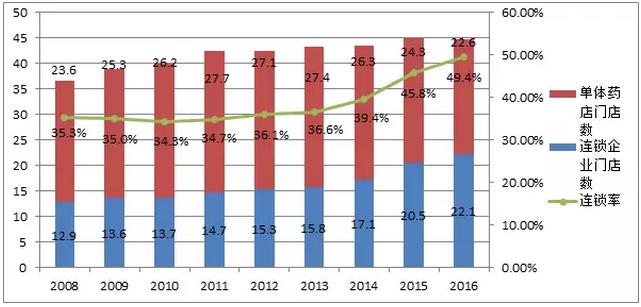

FIG. 3, 2008 ~ 2016, the number of stores (units: 10,000) and the rate of chain change in the retail chain

(data source: annual statistical report of CFDA)

From 2008 to 2016, the number of retail pharmacies in China has increased from 365,000 in 2008 to 447 thousand in 2016. Chain enterprises grew from 1985 to 5609 in 2016. At the same time, the number of single-drug pharmacies peaked in 2013 at a peak of 274, 000, with a total of 221, 000 in 2016.

The "capital acquisition" has become the high frequency word in recent years, and the trend of the industry scale, chaining and branding has already appeared. In 2008, the chain rate was 35.34 percent, up to 49.44 percent in 2016, with the industry concentration increasing year by year, but the gap with the 2/3 rate target was still in a relatively decentralized competitive situation.

2. The top 100 chain

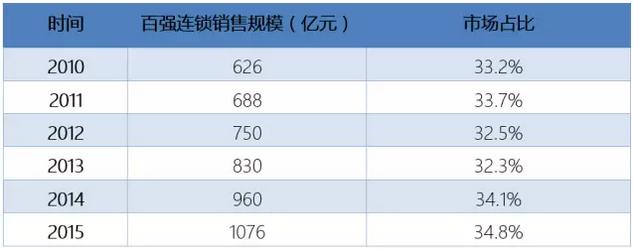

Table 1: top 100 sales volume and market share change in 2010 ~ 2015

From 2010 to 2015, the proportion of the top 100 is about 30%. It is too early for China's drug retail industry to talk about its oligarchic economy, compared with more than 75 per cent of the us retail market for CVS, Walgreens and Rite.

3. Capitalization

Table 2 changes in the size of the three major listed chains (sorted by listing order)

(source: annual report)

In 2014 ~ 2015, under the force of capital wind, the single-minded, yifeng and the people listed in a-share. It is worth noting that in 2016, the people's single-minded and common people's revenue exceeded the 6 billion yuan mark. Yifeng showed its advantages in growth, with revenue growth of 31.21 per cent in 2016.

In terms of the average single-store output dimension, the average single-store output and the growth rate of the common people are the best. In 2015 and 2016, the average single store output exceeded 3 million yuan, and in 2016, it increased 7.8% year on year. Yifeng followed suit, with average single-store output of more than 2 million yuan in two years, but declined year-on-year in 2016. The largest single-store chain, in 2016, saw its average single-store output rise slightly, to 2.7 percent.

Taken together, although the three major listed chain marketing network layout is not identical, "self-built + m&a" is the main way of their scale expansion. It is not hard to see that a new round of turf battles will become more intense, and in the push of capital, the concentration of China's drug retail market will also accelerate.

Besides three listed chain, strong mainstream chains have also opened a road of the capitalization: wash jade civilians, and Lin, the proper disclosed the prospectus of yunnan health, and in offering investment project will start in succession on the expansion of marketing network which stores: big intends to vote for 918 million yuan Lin, wash jade civilians will allocate 508 million yuan, the health of the poor will also plans to more than 400 million yuan on the construction of the chain drugstores to raise money for new.

The capital boom in drug retailing is, in the final analysis, an optimistic outlook for the industry. According to kang information released "2017 fighting talk: the blueprint of building industry decade", to social pharmacy as continues the main medicine separately under the premise of the next decade, drug retail terminal market scale will reach 1.72 trillion yuan (constant), accounting for about 65% of all drugs terminal market.

�� big and healthy development of the decade: people need

During the decade, the concept of big health was hot in the pharmaceutical retail industry. The awakening of self-medicated and self-care consciousness of residents is undoubtedly a new thought for the retail industry.

1. Self-medication

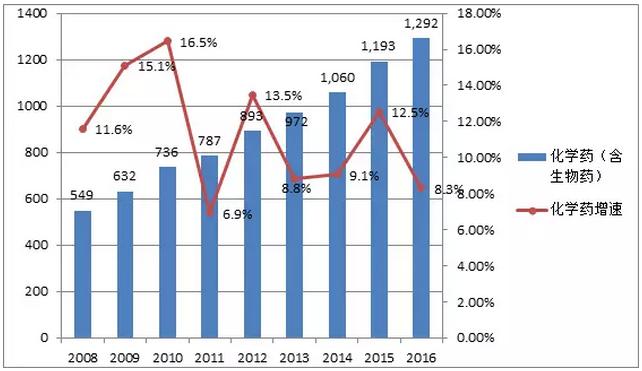

FIG. 4 market size of retail terminal chemical drugs (including biologics) in 2008 ~ 2016

(source: zhongkang CMH)

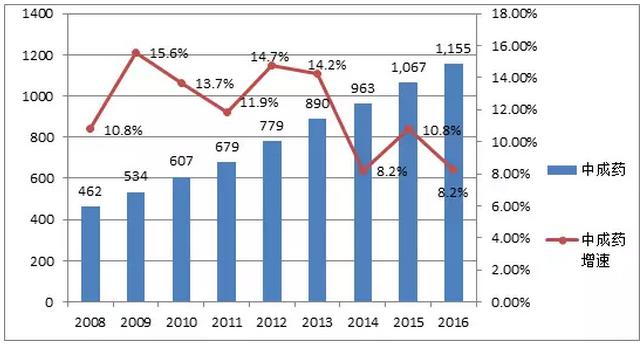

FIG. 5 market size of the market in the retail terminal between 2008 and 2016 (unit: billion yuan) and growth rate change

(source: zhongkang CMH)

Under the new health reform policy, retail pharmacies play an important role in improving drug accessibility. In fact, the sustainable growth of drug retail terminal, besides the policy dividend of new medical reform and health insurance coverage, is also benefited from the promotion and popularization of self-medication and self-care concept.

Specific to the drug category, chemical drugs (including biological drugs) increased from 54.9 billion yuan in 2008 to 129.2 billion yuan in 2016, and the number of Chinese medicines rose from 46.2 billion yuan in 2008 to 115.5 billion yuan in 2016.

2. Self-care

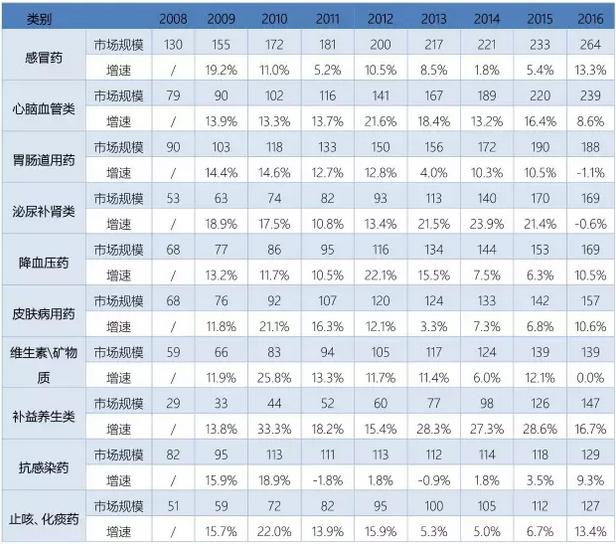

Table 3: the market size of the best-selling category of retail terminal (unit: billion yuan) and the growth rate of the retail terminal in 2008 ~ 2016

(source: zhongkang CMH)

As people living standard unceasing enhancement, our country residents self health care consciousness is growing, more and more residents from passive to active prevention, willingness to pay for health is increasingly strong.

From the top 10 best-selling segment of the retail terminal, the sales growth rate of the 2009/2016 supplement is always in double digits, and the market performance is especially outstanding compared with other categories. In particular, the average growth rate for 2009-2016 was 22.7 per cent, in particular, which is partly a sign of the growing awareness of consumer health management.

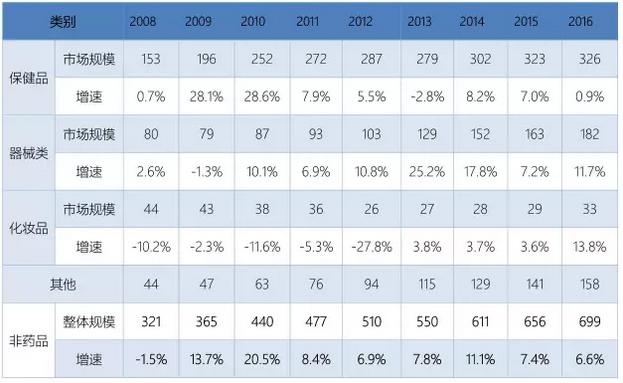

Table 4 2008 ~ 2016 retail terminal non-pharmaceutical and individual category scale (unit: 100 million yuan) and growth situation

(source: zhongkang CMH)

Retail pharmacies are also starting to focus on non-pharmaceutical products such as health care and equipment. According to the research data of China kang CMH, the non-pharmaceutical scale of the retail terminal grew at -1.5 percent in 2008, which began to grow rapidly in 2009 and reached its peak in 2010 of 20.5 percent in 2010.

In combination with the market background of the time, the policy of new health reform in 2009 on basic drugs, health insurance and primary care services has had a certain impact on the short-term operation of retail terminal. Under pressure to survive, many pharmacies have turned to diversification to find new profit points.

As a result of regulatory policies such as the GSP and a lack of successful business models, growth in non-drug sales has returned to single-digit growth after reaching its peak in 2010. The most intuitive is that in 2008 ~ 2012, the number of cosmetics sales that had been popular in pharmacies was negative. However, as the bulk of non-pharmaceutical products, the health products always occupy half of the non-pharmaceutical class, and after the negative growth in 2013, the health products maintain a slow growth.

But it is worth noting that in the same period, it is medicine issued by the size of the electric business growth, in 2012, Tmall medical library online, health care products, instruments, etc into the lion's share of the growth of online sales, according to the announcement that ali health as of the fiscal year ending March 31, 2017, more than 950 businesses in Tmall medicine sales platform blue cap health food, annual active buyers of more than 11.81 million, blue cap health food business turnover was about 2.772 billion yuan, is a growing awareness that means people self health care keeping in good health, and network consumption habits are formed.

�� prescription transfer: ten years prairie fire

Since the implementation of the reform, "medicine separation" has been mentioned repeatedly. The most intuitive effect of the separation of medicine is the prescription outflow, which will also refactor existing medical interests, and retail pharmacies are seen as the main beneficiaries of the change.

Prescription drugs

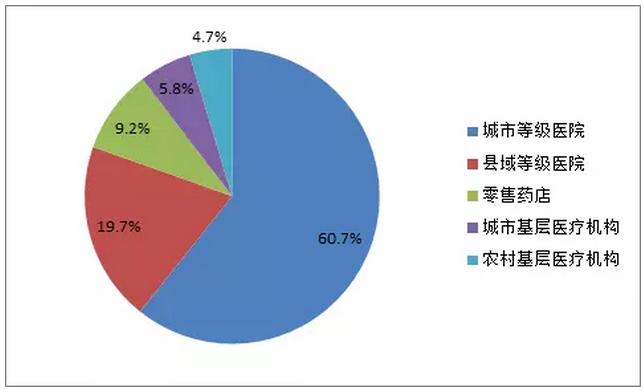

Figure 6. The market channel prescription drug share structure in 2016

(source: zhongkang CMH)

According to kang CMH data, from the point of the national drug market, 2016 grade hospital terminal (including city level hospital and county hospital) is still the main channel prescription drug sales, account for 80% of the market share; The retail terminal was followed by a 9.2 per cent share. Since the retail terminal's prescription mainly comes from hospitals, the growth of retail terminal prescription drugs is similar to that of hospital growth.

In recent years, it is not hard to see that retail pharmacy serves as the receiving party of the outflow prescription, and its role in the process of prescription outflow is being taken seriously. Is expected in the prescription under the impetus of the outflow of relevant policies, and the incidence of chronic diseases brought by the population aging increase under the influence of factors such as retail terminal will be squeezed out from the part of the hospital prescription, gradually increase market share.

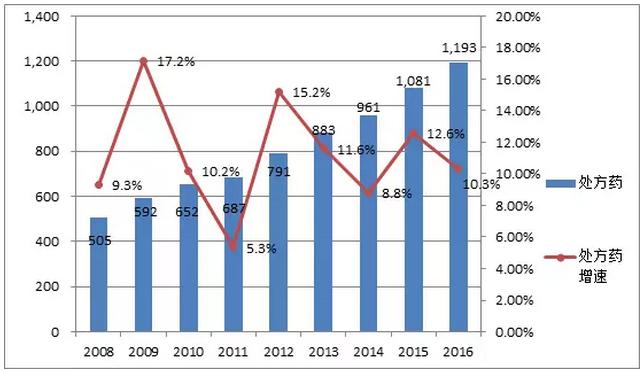

Figure 7: retail terminal prescription drug size (unit: billion yuan) and growth change in 2008 ~ 2016

(source: zhongkang CMH)

Figure 8: non-prescription drug size (unit: billion yuan) and growth change of retail terminal in 2008 ~ 2016

(source: zhongkang CMH)

Focusing on retail terminals, the prescription drug maintained a steady growth in 2008 ~ 2016, and the market share of retail terminals hovered around 47%. Since 2012, sales of prescription drugs have been growing faster than those of non-prescription drugs, according to the study. In 2016, sales of prescription drugs were still growing at a double-digit rate, higher than the overall growth rate of the retail terminal market, while non-prescription drugs were in weak growth (6.36%).

2. Health care store

In May 2017, the reform of the state council office issued the deepening the reform of medical health system 2017 key tasks, encourage the development of chain pharmacies, explore the prescribing information of medical institutions, health care billing info and drug retail spending connectivity, real-time information sharing. The health insurance information through, which means that the hospital's prescription circulation problem is paid attention to, it is a great benefit to the retail pharmacy to undertake the outflow prescription.

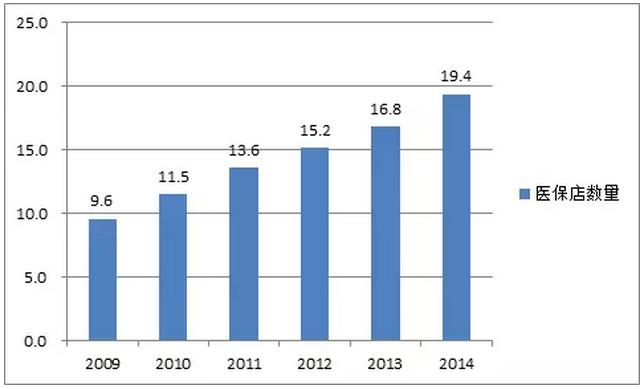

Figure 9: the number of health care stores in 2009 ~ 2014 (unit: 10,000)

(source: based on public information)

In the context of the separation of medicine, it can be said that the wide coverage of the designated drugstores is one of the foundations of the retail pharmacy to undertake the prescription outflow.

Between 2009 and 2014, the number of designated retail pharmacies nationwide rose from 96, 000 in 2009 to 194, 000 in 2014. The share of health care stores in the country rose from 24.7% in 2009 to 44.7% in 2014. With the implementation of the fixed-point agreement, the share of health care stores will have a greater improvement over the past two years. In Beijing, for example, by the end of 2016, there were 5,136 pharmacies in Beijing, but only 88 of those with designated medical insurance. With the implementation of the fixed-point agreement in Beijing in early 2017, the forecast will add 2,000 new medical care outlets.

�� profession ten years: people-oriented

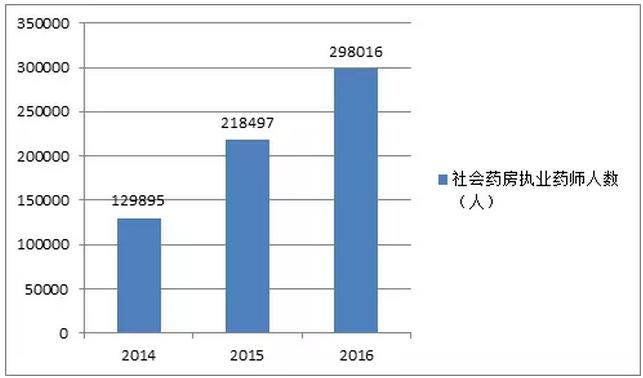

Figure 10 changes in the number of licensed pharmacists from 2014 to 2016

(source: national food and drug administration licensed pharmacist certification center)

After the cheap time, the drug retail industry specialization concept gradually returns. In addition, with the expected acceleration of the prescription outflow, the professional services of the short board, and under the GSP and other policies and regulations, the cultivation of professional talents, especially licensed pharmacists, is becoming more and more important. From 2014 to 2016, the number of licensed pharmacists in social pharmacy grew rapidly. The number of licensed pharmacists has more than doubled in 2016 compared with 2014, and the number of licensed pharmacists has risen from 0.3 to 0.7.

FIG. 11 the proportion of employees with different educational qualifications

(source: zhongkang research institute • pharmaceutical retail industry development research center)

Although specialized construction has become industry consensus, but to build the pharmacy professional team and to establish professional image is still blocked and long. According to kang information in 2017 by the new (Chinese pharmaceutical retail business innovation summit) published on the Chinese drug retailing specialized construction research report, 2017 chain enterprise staff degree distribution showed "two head small, middle small" olive shape features: bachelor degree or above and junior high school and the following two types of people, on average, accounted for only 9%; On average, the biggest is high school/secondary education, 47%; The second is a college degree, 35 percent.

The report also shows that the proportion of workers in the medical background is larger in the first-line stores, with 86 per cent of chain companies placing more than 75 per cent of their medical background staff in first-line stores.

But overall, the overall proportion of medical students in the background is 18%. Only 8 percent of the company's front-line employees are in the chain.

For the reasons that hinder the function of licensed pharmacists, the report shows that the highest proportion is the pharmacy assessment guide deviation and the lack of incentive measures, with 48% of the same degree. Secondly, the legal status is unclear, accounting for 22%; Once again, the existing business model conflicts with the store, accounting for 18%. But 32% of chain executives said there was no problem that pharmacists had trouble working. Visible, on the road of specialization of retail pharmacies, pharmacy internal business model, incentive system and external legislation guarantee, will largely influence the industry specialization process.

|